One of the original developers on the iSystem platform – Ilpo Kumpulainen of Ges Trading Strategies recently shared a piece with us looking at how value investing in the stock market has a corollary in the automated trading system world, and we found it so informative – we wanted to post it here… Enjoy:

_____________________________________________________________________________________________________________________________

A classic value investment style looks for stocks which are undervalued by the markets and go long if the fair value of a stock based on the futures earnings power is greater than their current market price. The key to success is to find stocks that contribute the most value within the timing of the investment. The strategy is simple, invest long-term and take advantage of short-term declines.

Can this same investment style be applied to trading systems?

The trading system equivalent to a stock being in ‘value mode’ and underpriced by the market is a system in drawdown. Many investors tend to buy stocks or enter into a trading system when they’ve been going up significantly. However, statistically, it can be argued that the best time to start trading a system is when it is in drawdown. The best “value” play can be buying on a dip like in stocks, because:

- The size of possible losses is reduced. In case the system has stopped working, an investor does not suffer the entire drawdown from the peak till it is detected that the system does no longer work (one can use the past historic drawdown amount as a way to measure when/if a system stops working).

- The probabilities for higher than average short-term returns are elevated as robust systems tend to revert back to their average returns after a drawdown.

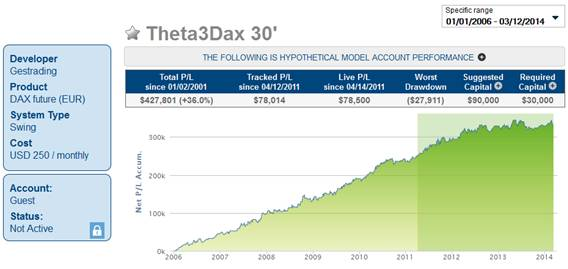

Let’s use system Theta3Dax to study a real life case. Theta3Dax has been trading live since 2011 and gives us a large sample size with which to test this “value” proposition:

Hypothetical Model Account Performance

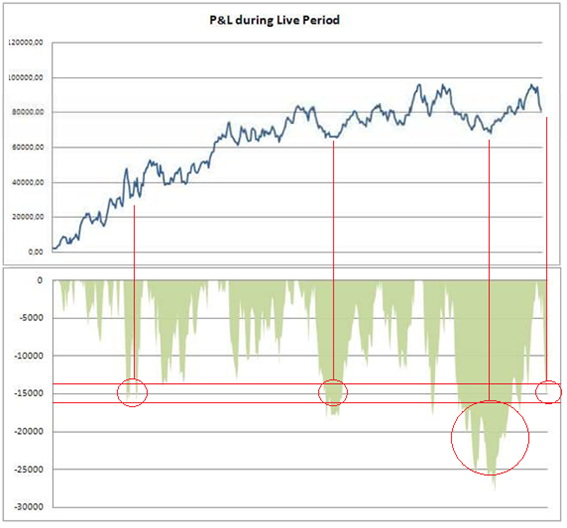

Let’s have a closer look on Theta3Dax’s live results and drawdowns:

Hypothetical Model Account Performance

As we can observe from the above graph, based on the past performance, the best time to start trading the system is when it is in a significant drawdown, with the program having come back from three separate major drawdowns (over $15k) since it has been traded by live clients. This does not always mean that immediate gains are right around the corner, however. For instance, the climb back from the 2013 drawdown took 2- 3 times longer than the past ones, and the drawdown went about 1.5 times further than the past ones due to market conditions in 2013 not being very favorable for the system.

So is a “value” approach right for you? You’ll have to decide that for yourself, and the above is only one approach to determine when to start trading a system. But as I look at it, value entry points like the system is offering currently present a lower risk opportunity to get in line with a system’s equity curve.

Disclaimer

The returns for trading systems listed above are hypothetical in that they represent returns in a model account. The model account rises or falls by the average single contract profit and loss achieved by clients trading actual money pursuant to the listed system’s trading signals on the appropriate dates (client fills), or if no actual client profit or loss available – by the hypothetical single contract profit and loss of trades generated by the system’s trading signals on that day in real time (real-time) less slippage, or if no real time profit or loss available – by the hypothetical single contract profit and loss of trades generated by running the system logic backwards on backadjusted data (backadjusted).

The hypothetical model account begins with the initial capital level listed, and is reset to that amount each month. The percentage returns reflect inclusion of commissions, fees, slippage, and the cost of the system. The monthly cost of the system is subtracted from the net profit/loss prior to calculating the percentage return.

If and when a trading system has an open trade, the returns are marked to market on a daily basis, using the backadjusted data available on the day the computer backtest was performed for backtested trades, and the closing price of the then front month contract for real time and client fill trades. For a trade which spans months, therefore, the gain or loss for the month ending with an open trade is the marked to market gain or loss (the month end price minus the entry price, and vice versa for short trades).

The actual percentage gains/losses experienced by investors will vary depending on many factors, including, but not limited to: starting account balances, market behavior, the duration and extent of investor’s participation (whether or not all signals are taken) in the specified system and money management techniques. Because of this, actual percentage gains/losses experienced by investors may be materially different than the percentage gains/losses as presented on this website.

Please read carefully the CFTC required disclaimer regarding hypothetical results below. HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN; IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR TRADING PROGRAM. ONE OF THE LIMITATIONS OF HYPOTHETICAL PERFORMANCE RESULTS IS THAT THEY ARE GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. IN ADDITION, HYPOTHETICAL TRADING DOES NOT INVOLVE FINANCIAL RISK, AND NO HYPOTHETICAL TRADING RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK OF ACTUAL TRADING. FOR EXAMPLE, THE ABILITY TO WITHSTAND LOSSES OR TO ADHERE TO A PARTICULAR TRADING PROGRAM IN SPITE OF TRADING LOSSES ARE MATERIAL POINTS WHICH CAN ALSO ADVERSELY AFFECT ACTUAL TRADING RESULTS. THERE ARE NUMEROUS OTHER FACTORS RELATED TO THE MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF ANY SPECIFIC TRADING PROGRAM WHICH CANNOT BE FULLY ACCOUNTED FOR IN THE PREPARATION OF HYPOTHETICAL PERFORMANCE RESULTS AND ALL WHICH CAN ADVERSELY AFFECT TRADING RESULTS.